Introduction

Machine learning algorithms are typically designed to make predictions or decisions based on patterns and relationships in data. Traditional approaches often rely on deterministic models, where parameters are fixed and assumed to be known or estimated from data using techniques like maximum likelihood estimation. However, in many real-world scenarios, there is uncertainty associated with both the data and the parameters of the model. Bayesian modeling and probabilistic programming offer a powerful framework for addressing this uncertainty by incorporating prior knowledge and updating beliefs in a principled way.

Bayesian Modeling

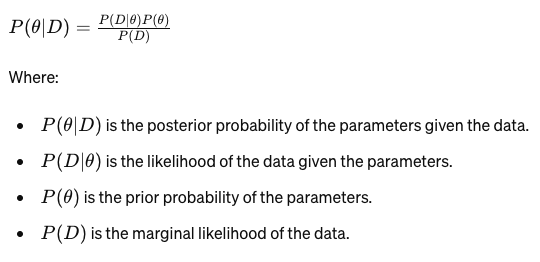

At the heart of Bayesian modeling is Bayes’ theorem, which provides a way to update our beliefs about a hypothesis (or model parameters) in light of new evidence (data). Mathematically, it can be expressed as:

In Bayesian modeling, we specify a prior distribution over the parameters, which represents our beliefs about their values before observing any data. Then, we update this prior distribution using Bayes’ theorem to obtain the posterior distribution, which reflects our updated beliefs after observing the data.

Probabilistic Programming

Probabilistic programming provides a high-level framework for specifying and performing Bayesian inference in complex probabilistic models. It allows users to describe probabilistic models using intuitive programming constructs, such as random variables and probabilistic functions, without having to manually derive and implement inference algorithms.

One popular probabilistic programming language is PyMC3, which provides a user-friendly interface for building and fitting Bayesian models. Let’s illustrate this with a simple example of Bayesian linear regression using PyMC3:

python

import pymc3 as pm

import numpy as np

import matplotlib.pyplot as pltnp.random.seed(42)

X = np.random.uniform(0, 10, 100)

true_slope = 2

true_intercept = 1

true_noise = 1

y = true_slope * X + true_intercept + np.random.normal(0, true_noise, 100)

with pm.Model() as model:

# Priors

slope = pm.Normal(‘slope’, mu=0, sd=10)

intercept = pm.Normal(‘intercept’, mu=0, sd=10)

noise = pm.HalfNormal(‘noise’, sd=1)

y_pred = slope * X + intercept

likelihood = pm.Normal(‘y’, mu=y_pred, sd=noise, observed=y)

trace = pm.sample(1000, tune=1000)

pm.traceplot(trace)

plt.show()

In this example, we specify a prior distribution for the slope, intercept, and noise parameters of the linear regression model. We then define a likelihood function that relates the observed data to the model parameters. Finally, we perform Markov chain Monte Carlo (MCMC) sampling to obtain samples from the posterior distribution of the parameters.

Conclusion

Bayesian modeling and probabilistic programming offer a flexible and principled approach to machine learning that is particularly well-suited for reasoning under uncertainty. By explicitly modeling uncertainty through probability distributions, these methods enable more robust decision-making and allow practitioners to incorporate prior knowledge into their analyses.

In this article, we’ve explored the fundamentals of Bayesian modeling, including Bayes’ theorem and the concept of posterior inference. We’ve also introduced probabilistic programming as a powerful tool for implementing Bayesian models, with examples using PyMC3.

As machine learning continues to evolve, Bayesian methods and probabilistic programming are likely to play an increasingly important role, particularly in domains where uncertainty quantification is critical, such as finance, healthcare, and autonomous systems. By embracing these techniques, practitioners can build more reliable and interpretable machine learning models, ultimately leading to more informed decision-making and better outcomes.